In support of active fund management

This is the time for active managers to shine

Opportunity is ripe for active investors

Don’t ‘buy the index’: Investing in the time of the coronavirus

Stockpickers can prove their worth in crisis, says Aberdeen

It’s a Weird Market. Time To Go Active.

A selection of headlines from publications in Australia and around the world. This has been the message since COVID-19 took off. Active managers are once again ready to step into the light and prove their worth in volatile investment markets.

It’s a cycle as old as time. You can set your watch by it. A new year rolls around or maybe there’s some market volatility. These articles start coming thick and fast. Active fund managers with good teeth and $100 haircuts are being fawned over by journalists. This is the time we’ll need their expertise. This year is different, with new challenges. This market has changed. We’ll all need to be selective to conquer it.

They must assume we’re all goldfish.

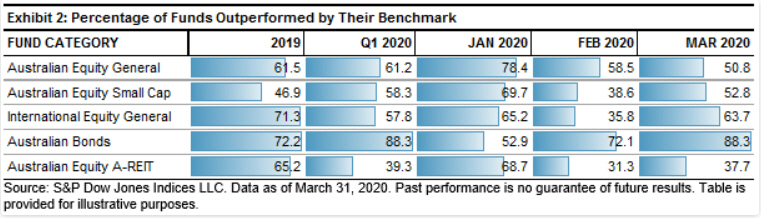

Conveniently absent from the media right now, their performance against the market. SPIVA, the data keepers of the active managers vs index debate put out a special release last week. Looking at how active managers performed recently. How did their expertise in volatile markets work out?

The first quarter tells the story. Apart from a significant difference in listed real estate, the supposed ability of active managers to outperform in these volatile conditions hasn’t eventuated. In the Australian general equity space 61.5% of active managers were outperformed by the benchmark in 2019. Almost in line with quarter 1 2020, with 61.2% of active managers outperformed by their benchmark.

How have they performed in the recovery? Not sure. Many investors were wringing their hands about further falls. Lately the market has kept moving upward. It’s only an assumption, but one might think those most likely to be sitting out the rally are active managers. The indexes certainly haven’t missed it. And they haven’t missed it for a long time. Leaving active managers in their dust.

The bravado to keep fronting up. In the face of all the data. To keep saying “this will be our time”. Their persistence would be admirable. If it weren’t for the fact their mythmaking is costing investors dearly.

Back in March, SPIVA released their 2019 results. For the most part, they were missed in the COVID-19 drama. Looking at the figures, the story becomes even more damning.

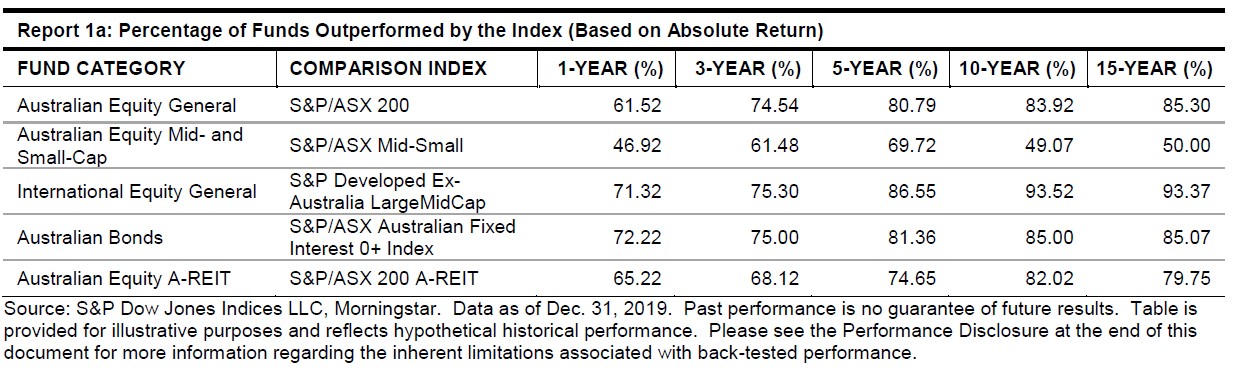

As time goes on, the odds of finding an active manager who can outperform their benchmark narrow. The only area where it’s a coin flip that you might snag an outperforming active manager is in the mid-small cap space. Across the board, the odds are abysmal. An investor is better off using low-fee index funds to construct their portfolio according to their goals.

The data backs this up. It is a simple story. It almost writes itself. In the age where the media is crunched for time, it should be a no brainer to write. But barely a peep. Why?

Some speculation.

The spend. That extra 1% active managers charge helps to employ PR people and it buys advertising. A little kick along for the never-ending narrative that “active managers are about to shine”.

The excitement. Look at this story. It’s built on two tables of data. How does it compete with some guy with big teeth, a slick haircut and nice tan, photographed in a boardroom that overlooks Sydney Harbour? 1000 words of energy as he talks with certainty about his picks and future forecasts? Mind you, if he had a booth at the local fair charging $10 for tarot card readings the same journalists wouldn’t give him the time of day.

In the next crisis we hope to see the following headlines:

Stockpickers won’t prove their worth in crisis

It’s a Weird Market. Don’t Go Active.

Do ‘buy the index’

Opportunity is ripe for index investors

Those will be the headlines consistent with facts and reality.