“Have you seen the price of gold?”

“What about gold?”

“Is there a reason you don’t invest in gold?

These are common but also intermittent questions. An investment that has recently increased in value will receive attention. Its proponents will talk about it. The media will cover it. People want to know more about it. This waxes and wanes. Middling performance isn’t so exciting. It doesn’t attract attention. People don’t want to know. Gold is up right now. People want to know.

Unlike various other investments that emerge, we don’t dispute gold’s legitimate status as an asset or a commodity. Does it have a place in your portfolio?

We have rules when building portfolios. Understanding the risk/return characteristics of assets. Shares. Listed property. Fixed interest. Cash. There are clear evidence-based reasons to hold those four asset classes in a portfolio. A properly managed portfolio requires rules around construction and management.

Data shows investment markets have continued to work for centuries. Every imaginable scenario. Various factors such as small and value segments of the market have shown to outperform over the longer term. Though those performance factors aren’t always present. On the defensive side, fixed interest has credit and term risk which can affect returns. That, along with the cash, exist to provide liquidity when markets are volatile.

One part of a portfolio aims to offer growth and some income. Stability, liquidity and some income from the other part. The ratio of these assets within a portfolio explains its performance. Younger, growing a portfolio and want to take more risk? You tilt it to the growth side. Older, looking to draw from your portfolio and want stability? You tilt it to the defensive side.

Proponents of gold use various arguments to justify its position as a must have investment. A hedge against inflation. A safe haven in times of calamity. An alternative to assets with low returns. Where does gold fit? Is it a growth asset or a defensive asset?

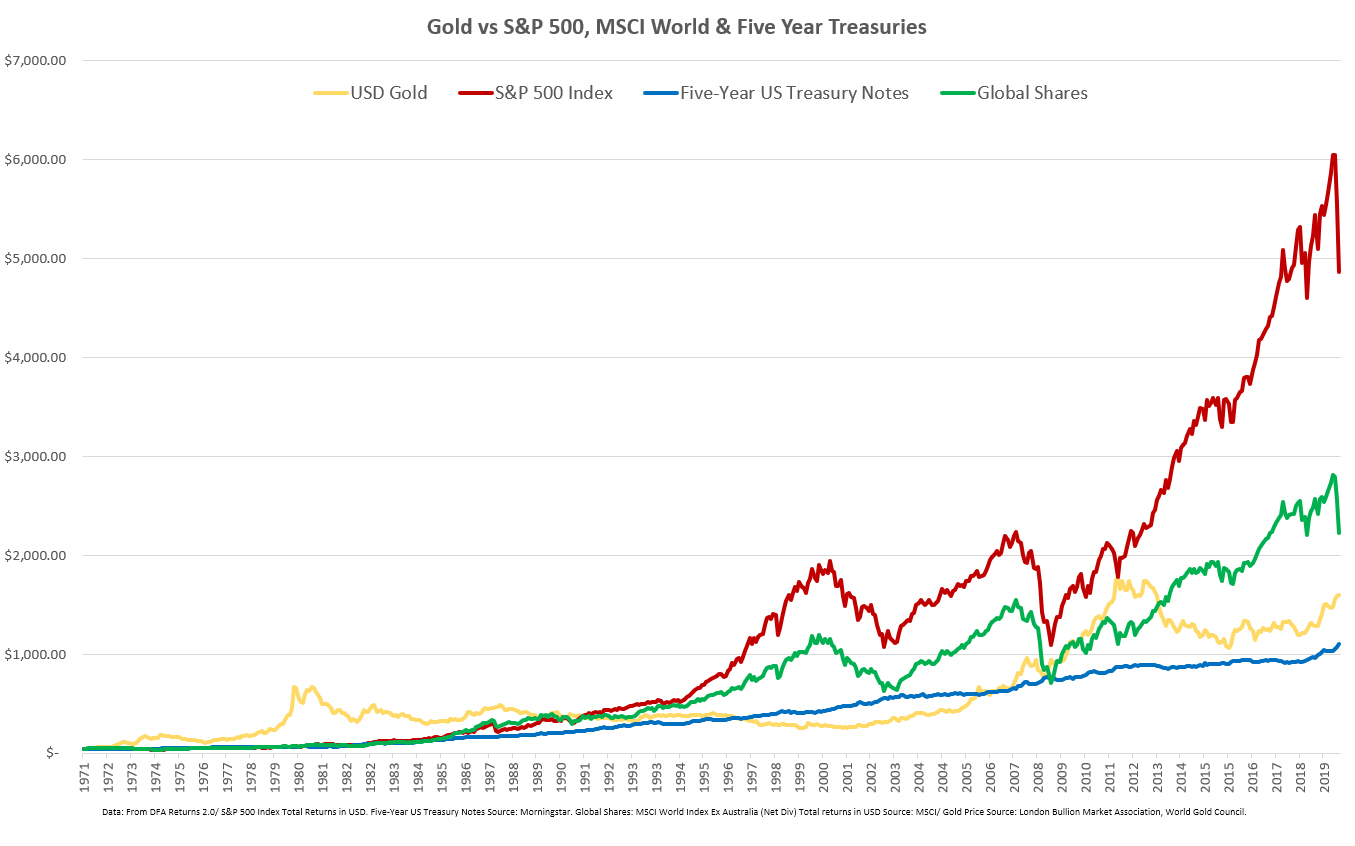

A long run chart can provide some perspective.

The chart shows an ounce of gold against the same value invested in the S&P 500, and Five-Year Treasury notes (fixed interest) in US dollars. The start date is when the US abandoned the gold standard in December 1971. The end date is March this year.

It’s indisputable. Gold has enjoyed some periods of outstanding performance. The 1970’s was a great time to be in gold. It culminated with a big high in 1980. Unfortunately, anyone piling in and thinking of future riches was forced to wait another 27 years to reclaim their previous highs. Gold’s next big decade kicked off in the 2000’s. That culminated with its most recent high in September 2011. While gold has enjoyed a good run since September 2018, it’s still yet to regain that September 2011 high.

Measured against a sharemarket index, like the S&P 500, gold is still very much trailing in long term wealth creation. It’s a similar story against a world sharemarket index. There’s been no comparison. So maybe gold’s not a growth asset? Long term against fixed interest, gold has proven a better prospect. Yet as a defensive, it’s proven to be significantly more volatile and without the benefit of an income stream.

We’d argue gold falls into a speculative area around currency. The impulse to own gold (beyond seeing it recently increase in value) is often motivated by a response to current events or an expectation of economic calamity. Proponents will often suggest currency is being devalued and gold will remain as the true store of wealth.

Asserting an asset be held because it will emerge as a store of value in a crisis is a speculative forecast. Yet it is one people clearly believe. During times of concern the price of gold increases. With the coast clear, the price decreases or has long periods of stagnation. It appears investors abandon it.

It’s something of a chicken or egg scenario. Is gold increasing in price because it is genuinely more valuable in a crisis? Or are people now attuned to buy in and push up the price because they believe it will become more valuable? We’re still not sure.

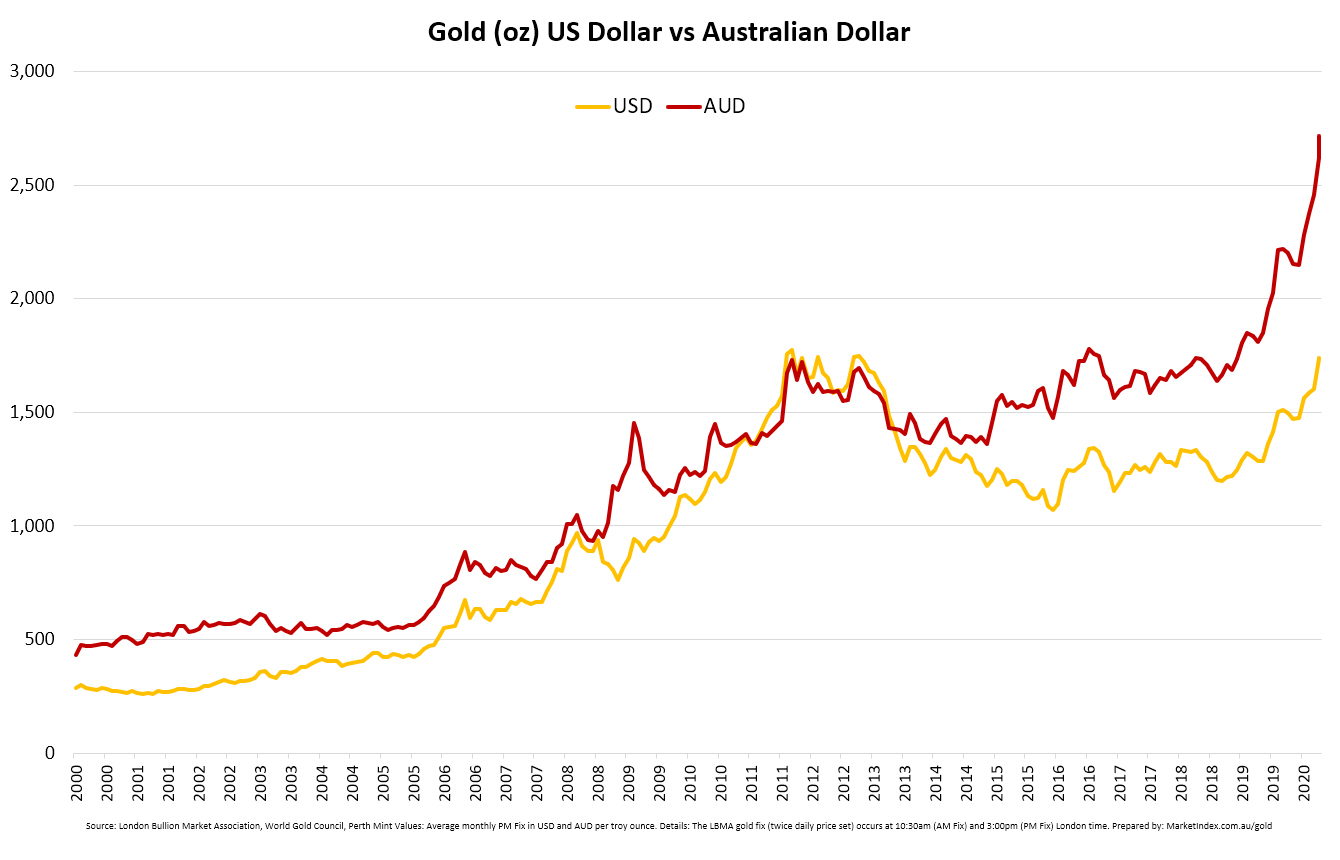

There’s a secondary element that needs addressing. Currency. To this point we’ve highlighted the price of gold in US dollars. In US dollar terms, the gold price is still below its 2011 highs. In Australian dollar terms gold is at an all-time high. Since its peak early last decade, the Australian dollar has steadily lost value against the US dollar. Initially the falling dollar helped shield gold’s price from any decline. It then propelled gold’s price higher.

This is another element Australian gold investors need to factor. Do they take a position on the currency? Over the past few years there have been Australian dollar forecasts ranging from 40 to 80 cents. Who to believe? The currency won’t always act as a tailwind.

Currency movement is another risk to be managed. To more prudently manage this risk, we hedge part of our global portfolios to protect against currency fluctuations. This circles back to a point we made earlier. We have a set of rules around investing. There’s no room for economic or currency forecasts. At best they’re always a guess. We believe the rules used offer the best opportunity to build wealth and provide income over the long-term, while managing risk.

We’re not convinced on gold as an asset class to hold. A forecast or a ‘what if’ scenario is never a compelling reason to hold an asset. However, some investors will always have the urge to speculate. If that’s you, keep something in mind. One of the world’s better-known proponents of gold is Peter Schiff. Schiff has forecast gold to hit $5,000. He was even saying this when gold was at an all time high in 2011.

What’s Peter Schiff’s position on gold in an investor’s portfolio? Hold 5-10% in gold. That’s it!

That should tell you something. We’ve encountered investors who want to hold 50-100% of their money in gold! Understand, it’s a speculative asset subject to currency fluctuations. As Schiff forecasts, it might go to $5,000. Alternatively, it might go nowhere for 27 years.

Owning a small amount as a speculative endeavour? To satisfy your own curiosity? Purchased with money you don’t need in the short term? Probably not going to cause any harm. At times you’re likely to feel great about owning it. Other times you’ll be frustrated by it.

No one asset is likely to be the panacea to your investment woes.