Alpha. In an investment sense it means how much better your returns were against a specific benchmark. If you were holding an ASX small cap fund and it returned 12% while the ASX small cap index returned 10%, your alpha is 2%. This can also work in reverse. Your fund returns 8% while the index returned 10%, well you’ve got negative alpha of 2%.

The financial industry has long been attempting to get to the bottom of what alpha is within financial advice. Someone pays a financial adviser X amount, does that person derive more in value from that advice than they pay out?

Fund manager Vanguard has tried to quantify this value for years with an ongoing report called ‘Adviser Alpha’. Their most recent report had defined three areas of value. They say these three areas can combine to add 3% to someone’s bottom line.

Portfolio: building and maintaining a portfolio for the investor accounting for tax, fees and rebalancing.

Financial: saving, debt, cashflow and retirement planning, along with insurance and estate planning.

Emotional: trust in the adviser, maintaining confidence in the plan and ensuring discipline so the investor makes it through any rough markets or periods of poor performance which are inevitable.

Some of these are subjective, how does someone value trust and peace of mind? Meaning value will always come down to individual circumstances. Further, what an adviser delivers to one person will be different to what the same adviser delivers to someone else.

Every adviser has instances where clients have been tempted by an untested investment. It was a sober second opinion that saved tens of thousands in losses and tens of thousands more in opportunity cost. Similarly, many advisers have a story where they’ve counselled a client out of cancelling insurance. Months later that client had a life changing diagnosis.

Other clients will never need a second opinion, nor will they question their insurance. Do they receive the same value? Maybe that shows trust in the adviser and the strategy laid out. If an investor is listening to their adviser and following through, that’s why they engaged an adviser – advice and a plan to follow. Beyond that, clients need to ask could they manage their own financial affairs as effectively and more importantly – do they really want to?

One of the biggest challenges financial advisers have always faced is ensuring clients adhere to their plans. We’re all human and prone to second guessing or panicking. Good financial advice is never offered as an offhand suggestion. Good advice comes after an examination of a person’s affairs. It’s provided as a prescription to improve their financials and define a strategy to reach their goals.

What’s the result when clients don’t listen or make changes to their strategy?

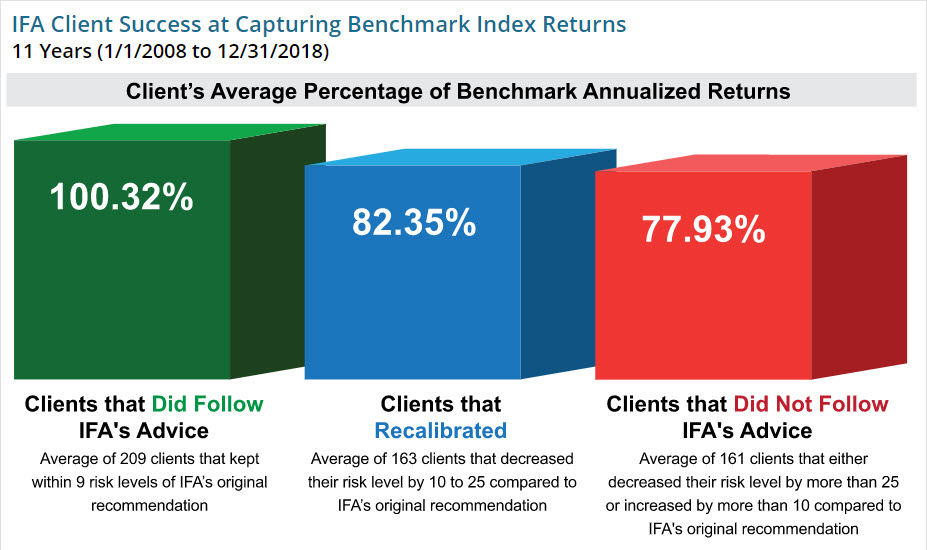

Index Fund Advisors (IFA) a financial advisory firm in the US can tell us. IFA examined their client base to better understand what it might cost someone who doesn’t listen or wants to make their own changes to a recommended portfolio. IFA measured over 500 of their client’s portfolios from the beginning of 2008 until the end of 2018.

Of the 533 client portfolios measured, 209 clients followed IFA’s advice and kept close to their original recommended portfolio. 163 clients moved away from their recommended portfolio, decreasing their stock allocations between 10% to 25%. 161 clients moved away from their recommended portfolio, lowering their allocation to stocks by more than 25% or increasing their allocation by more than 10%.

The outcomes were telling. Averaged out, the clients who followed IFA’s advice beat their benchmark by 0.32% over the 11 years. The average of the clients who mildly diverted from IFA’s advice underperformed their benchmark by 17.65%, while the average of the clients who majorly diverted from IFA’s advice underperformed their benchmark by 22.07%.

Here are some simple calculations to illustrate these outcomes in monetary terms. Assume three investors had $100,000 invested back in 2008 without further contributions or withdrawals and their benchmark returned 100% in that 11 years or 6.50% per annum.

The first investor followed their adviser’s strategy through every bump and hurdle. Their portfolio returned 100.32% or 6.52% per annum over the 11 years, turning $100,000 into $200,320.

The second investor wasn’t as convinced by their adviser. They made some changes, their portfolio returned 83.35% or 5.61% over the 11 years, turning $100,000 into $183,350.

The third investor was even less convinced by their adviser. They made even bigger changes, their portfolio returned 77.93% or 5.38% per annum over the 11 years, turning $100,000 into $177,930.

As this shows, there can be a cost when investors divert from a customised portfolio – their returns suffer. While we say not to chase returns, returns matter when they’re aligned with an investor’s goals. A good portfolio will be constructed according to the risk an investor needs to take to achieve their goals. While there is never any guarantee on returns, if an investor makes changes, they’re less likely to sail into their intended port within their expected time frame.

In the short term, a change in strategy or new investment option always projects a gleaming façade of safety, savings or promise. It’s only a long-term weathering that determines the options that are truly rust proof and built for purpose. Unfortunately, the bleak reality of IFA’s study highlights 60% of the clients tracked couldn’t help but make changes.

There are a lot of temptations and distractions out there. Financial decisions are packed with emotion. If an adviser can keep an investor on track it goes a long way to defining that alpha.